Understanding Basic Investment Attributes

Embarking on the world of investing can feel overwhelming, but grasping a few core attributes is crucial for building a solid financial future. These attributes serve as guidelines, helping you evaluate investment opportunities and align them with your personal goals and risk tolerance.

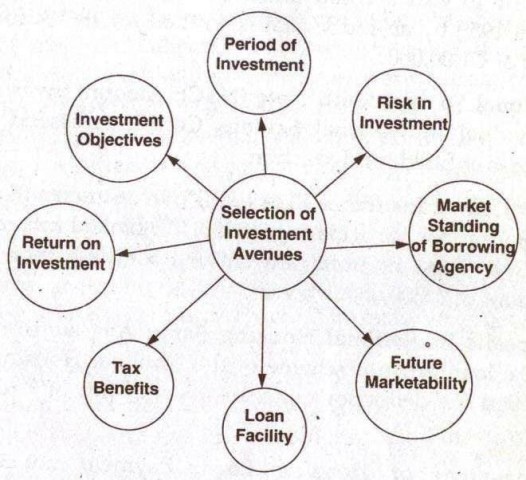

Risk and Return: The Fundamental Trade-off

The relationship between risk and return is the cornerstone of investment. Higher potential returns typically come with higher risk, and vice versa. “Risk” refers to the uncertainty of achieving the expected return. Investments perceived as safe, like government bonds, generally offer lower returns. Conversely, investments with greater potential for growth, such as stocks (especially those of smaller companies), involve higher volatility and the possibility of losing capital. Understanding your risk tolerance is key to selecting appropriate investments. Are you comfortable with the possibility of losing a portion of your investment for the chance of higher gains? Or do you prioritize capital preservation above all else?

Liquidity: Accessing Your Funds

Liquidity refers to how easily an investment can be converted into cash without significant loss of value. Cash itself is the most liquid asset. Stocks and publicly traded bonds are generally considered liquid because they can be bought and sold relatively quickly on exchanges. Real estate, on the other hand, is an illiquid asset. Selling a property can take time and involves transaction costs. Liquidity is an important consideration based on your financial needs. Do you need easy access to your invested funds? If so, prioritize liquid assets.

Time Horizon: The Power of Compounding

Your time horizon, the length of time you plan to hold an investment, significantly impacts your investment strategy. A longer time horizon allows you to weather market fluctuations and benefit from the power of compounding. Compounding occurs when the earnings from an investment are reinvested, generating further earnings. Over time, this snowball effect can dramatically increase your returns. With a long time horizon (e.g., decades until retirement), you can afford to take on more risk in pursuit of higher returns. Shorter time horizons require a more conservative approach to minimize potential losses.

Diversification: Spreading the Risk

Diversification is the practice of spreading your investments across different asset classes, industries, and geographies. The primary goal is to reduce the overall risk of your portfolio. By not putting all your eggs in one basket, you mitigate the impact of any single investment performing poorly. A diversified portfolio might include stocks, bonds, real estate, and commodities. The optimal level of diversification depends on your individual circumstances, but it’s generally a sound strategy for managing risk.

Inflation: Preserving Purchasing Power

Inflation erodes the purchasing power of your money over time. It’s essential to consider inflation when evaluating investment returns. An investment that yields a nominal return of 3% per year might not be sufficient if inflation is running at 2% per year, as your real return (after accounting for inflation) is only 1%. Investments that have the potential to outpace inflation, such as stocks and real estate, can help preserve your wealth in the long run.

By carefully considering these basic investment attributes, you can make more informed decisions and build a portfolio that aligns with your financial goals and risk tolerance. Remember, investing is a long-term game, and a well-thought-out strategy is essential for success.

600×200 basic investment styles gurpreet saluja from www.gurpreetsaluja.com

600×200 basic investment styles gurpreet saluja from www.gurpreetsaluja.com  961×930 investment analysis evaluation attributes efm from efinancemanagement.com

961×930 investment analysis evaluation attributes efm from efinancemanagement.com  600×455 fb investors investment criteria from fbinvestors.com

600×455 fb investors investment criteria from fbinvestors.com  526×480 investment attributes bms bachelor management from www.bms.co.in

526×480 investment attributes bms bachelor management from www.bms.co.in  600×900 basic investment concepts leo ly money coach from www.isaved5k.com

600×900 basic investment concepts leo ly money coach from www.isaved5k.com  843×459 hierarchy investment importance prioritising from cleartax.in

843×459 hierarchy investment importance prioritising from cleartax.in  1000×1835 developing good investment habits chin family from www.ifec.org.hk

1000×1835 developing good investment habits chin family from www.ifec.org.hk  500×500 investment characteristics features importance from commercemates.com

500×500 investment characteristics features importance from commercemates.com