Monte Carlo Simulation in Excel for Finance

Monte Carlo simulation is a powerful technique used in finance to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random variables. It allows you to see the range of potential outcomes and the likelihood of each. Using Microsoft Excel, even users with limited programming experience can leverage this technique to make more informed financial decisions.

How it Works

The core principle involves building a model of the financial situation you’re interested in, such as investment returns, portfolio performance, or project profitability. Within this model, you identify the key variables that are subject to uncertainty. These variables are then assigned probability distributions, representing the range of possible values they could take on. Common distributions include normal, uniform, triangular, and lognormal, each suited to different types of uncertainty.

Excel’s built-in functions, such as RAND() and NORMINV(), are crucial. RAND() generates a random number between 0 and 1. This random number is then used with distribution-specific inverse functions (like NORMINV() for the normal distribution) to generate a random value based on the defined probability distribution for that specific variable. For example, if you’re modeling stock price volatility and assume it follows a normal distribution with a mean of 10% and standard deviation of 5%, NORMINV(RAND(), 0.10, 0.05) will generate a random volatility rate for each simulation.

The simulation then runs iteratively, typically thousands of times. In each iteration, a new set of random values is generated for each uncertain variable based on their defined distributions. These values are fed into the model, and the resulting outcome (e.g., portfolio value, project NPV) is recorded. After all iterations are complete, the recorded outcomes are analyzed to generate a distribution of possible results. This distribution allows you to visualize the potential range of outcomes and estimate the probability of achieving specific targets.

Building a Simple Model

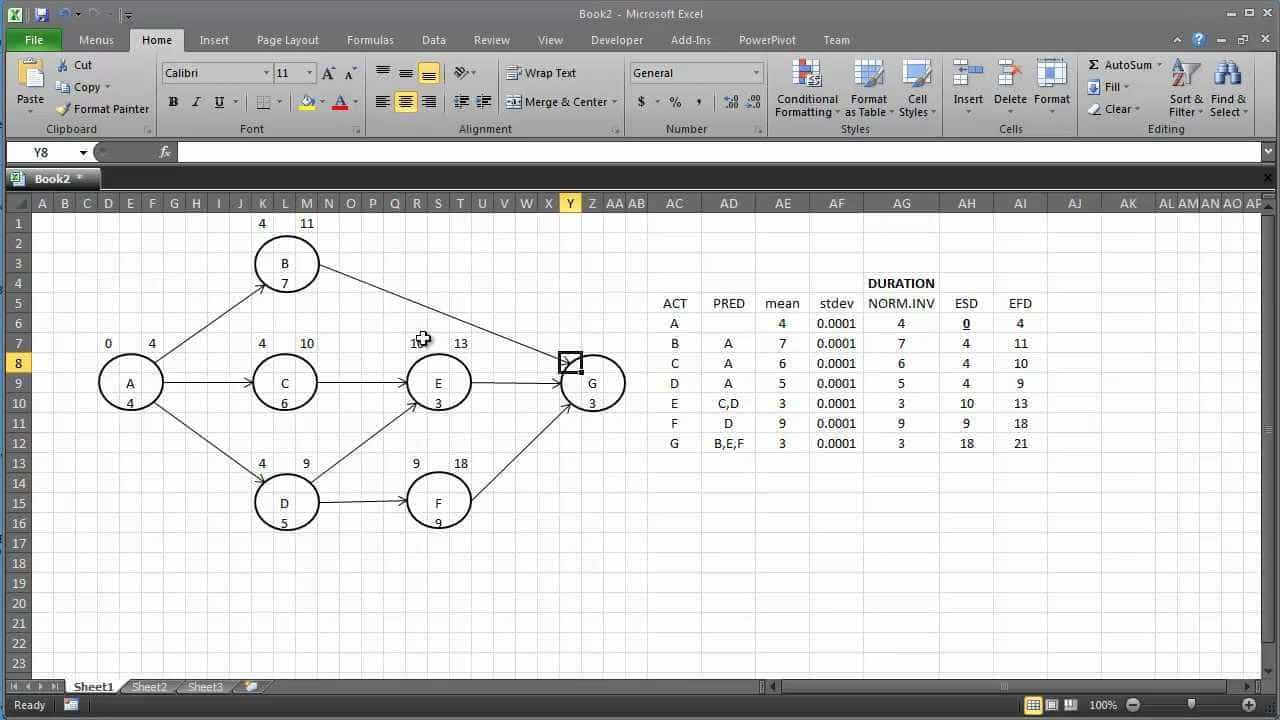

1. **Define your model:** Set up your spreadsheet with clear inputs (e.g., initial investment, growth rates, costs) and formulas that calculate the desired output (e.g., final value, profit).

2. **Identify uncertain variables:** Determine which inputs are uncertain and need to be modeled with distributions.

3. **Assign probability distributions:** Choose the appropriate distribution for each uncertain variable and define its parameters (e.g., mean, standard deviation, minimum, maximum).

4. **Implement random number generation:** Use Excel functions like RAND() and distribution-specific inverse functions to generate random values for each uncertain variable in each simulation iteration.

5. **Run the simulation:** Use Excel’s data table feature to automatically run the model multiple times, each time with a different set of random inputs. The data table should record the outcome you are interested in for each iteration.

6. **Analyze the results:** Create histograms and calculate statistics (e.g., mean, standard deviation, percentiles) from the recorded outcomes to understand the distribution of possible results and the probabilities of achieving specific targets. Excel’s charting tools are invaluable here.

Benefits

Monte Carlo simulation provides a more realistic picture of potential outcomes compared to single-point estimates. It helps in risk assessment, scenario planning, and making more robust financial decisions. By visualizing the range of possibilities, you can better understand the potential downsides and upsides, and adjust your strategies accordingly.

Limitations

The accuracy of the simulation depends heavily on the quality of the model and the appropriateness of the chosen probability distributions. It’s crucial to carefully consider the underlying assumptions and data used in the model. Additionally, Excel-based simulations can become computationally intensive for complex models with many uncertain variables and iterations, potentially requiring external add-ins for performance improvements.

1024×929 montecarlo excel maven from www.excelmaven.com

1024×929 montecarlo excel maven from www.excelmaven.com  1280×720 monte carlo simulation spreadsheet monte carlo simulation from db-excel.com

1280×720 monte carlo simulation spreadsheet monte carlo simulation from db-excel.com  1920×908 monte carlo simulation excel template eloquens from www.eloquens.com

1920×908 monte carlo simulation excel template eloquens from www.eloquens.com  790×513 monte carlo simulation excel marketxls add formulae from marketxls.com

790×513 monte carlo simulation excel marketxls add formulae from marketxls.com  150×150 monte carlo option pricing excel from investexcel.net

150×150 monte carlo option pricing excel from investexcel.net  1920×910 monte carlo simulation excel model eloquens from www.eloquens.com

1920×910 monte carlo simulation excel model eloquens from www.eloquens.com  880×594 monte carlo simulation excel eloquens from www.eloquens.com

880×594 monte carlo simulation excel eloquens from www.eloquens.com  1700×817 investment return monte carlo simulation excel model template eloquens from www.eloquens.com

1700×817 investment return monte carlo simulation excel model template eloquens from www.eloquens.com  760×367 monte carlo simulations excel financetrainingcoursecom from financetrainingcourse.com

760×367 monte carlo simulations excel financetrainingcoursecom from financetrainingcourse.com  720×540 monte carlo analysis macros excel model eloquens from www.eloquens.com

720×540 monte carlo analysis macros excel model eloquens from www.eloquens.com  1280×720 monte carlo excel template hq printable documents from whoamuu.blogspot.com

1280×720 monte carlo excel template hq printable documents from whoamuu.blogspot.com  1050×700 monte carlo simulation excel template financial analyst from 365financialanalyst.com

1050×700 monte carlo simulation excel template financial analyst from 365financialanalyst.com