Age-Based Investment Strategies: A Guide

Your age is a crucial factor in determining the most suitable investment strategy. As time horizons shorten and risk tolerance potentially decreases, investment approaches should adapt accordingly. This guide explores age-based investment options, providing a roadmap for financial planning throughout different life stages.

Young Adults (20s-30s): Growth Focus

In your 20s and 30s, time is your greatest asset. With decades until retirement, you can afford to take on more risk to pursue higher potential returns. The primary goal is to maximize growth.

- Stocks: Allocate a significant portion of your portfolio to stocks, especially growth stocks and emerging market equities. These offer the highest potential for long-term capital appreciation. Consider investing in a diversified stock market index fund or ETF to minimize risk.

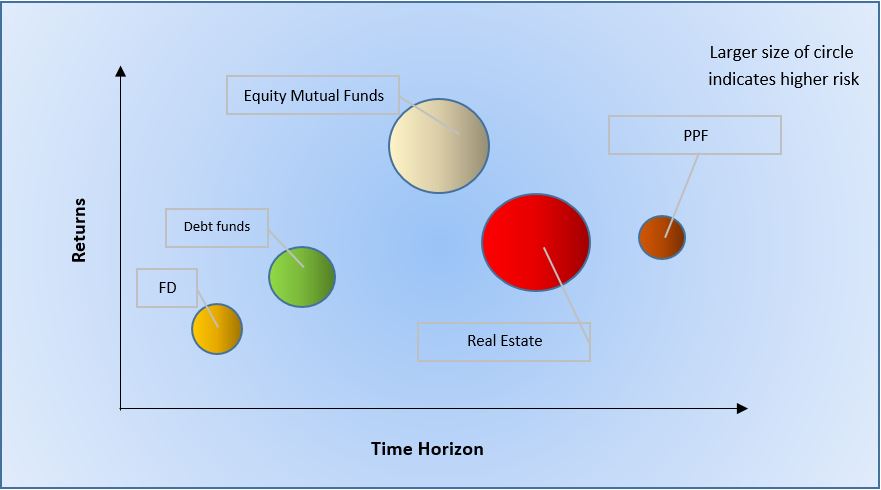

- Real Estate: Investing in a home can be a smart move, building equity over time. Consider rental properties as a potential passive income stream, but carefully assess the risks and responsibilities of property management.

- Early Retirement Accounts: Maximize contributions to tax-advantaged retirement accounts like 401(k)s and Roth IRAs. Take advantage of employer matching programs.

- Alternative Investments: A small allocation (5-10%) to alternative investments like venture capital or private equity might be considered, but only if you have a high-risk tolerance and understand the illiquidity involved. Proceed with caution.

Mid-Career (40s-50s): Balancing Growth and Stability

As you approach mid-career, it’s time to strike a balance between growth and capital preservation. Your retirement horizon is closer, and you need to protect the gains you’ve made while still growing your wealth.

- Balanced Portfolio: Shift towards a more balanced portfolio with a mix of stocks and bonds. Gradually reduce your stock allocation and increase your bond allocation to lower overall portfolio volatility. Consider a target-date fund that automatically adjusts the asset allocation as you near retirement.

- Real Estate: Continue paying down your mortgage and consider diversifying your real estate holdings. Explore options like REITs (Real Estate Investment Trusts) for passive income.

- Debt Management: Prioritize paying off high-interest debt, such as credit card debt.

- Tax Optimization: Focus on tax-efficient investing strategies to minimize taxes on your investment gains.

Pre-Retirement and Retirement (60s+): Income and Preservation

In the years leading up to and during retirement, the focus shifts to generating income and preserving your capital. Risk tolerance is generally lower, and the need for a reliable income stream becomes paramount.

- Conservative Portfolio: Maintain a conservative portfolio with a larger allocation to bonds, dividend-paying stocks, and other income-producing assets.

- Fixed Income Investments: Consider investing in government bonds, corporate bonds, and municipal bonds to generate a steady stream of income.

- Annuities: Explore the possibility of purchasing an annuity to provide a guaranteed income stream for life. Consider different types of annuities and their associated fees.

- Withdrawal Strategy: Develop a well-defined withdrawal strategy to ensure your savings last throughout your retirement. A common guideline is the “4% rule,” but it’s essential to adjust this based on your individual circumstances.

- Healthcare Planning: Plan for healthcare expenses, including Medicare and supplemental insurance.

Important Considerations

This is a general guide, and your individual investment strategy should be tailored to your specific circumstances, risk tolerance, financial goals, and time horizon. It’s always recommended to consult with a qualified financial advisor to create a personalized investment plan.

700×510 investment options salaried individuals web itb group news from webitbgroup.com

700×510 investment options salaried individuals web itb group news from webitbgroup.com  720×399 investment options beginners professionals from moneyconnexion.com

720×399 investment options beginners professionals from moneyconnexion.com  1080×2220 aggressive investment options info investment business ideas from investmentbusinessideas.blogspot.com

1080×2220 aggressive investment options info investment business ideas from investmentbusinessideas.blogspot.com  881×490 investment options professionals told from officechai.com

881×490 investment options professionals told from officechai.com  550×425 investment options india from moneyexcel.com

550×425 investment options india from moneyexcel.com  600×450 investment options nigeria nigerian finder from nigerianfinder.com

600×450 investment options nigeria nigerian finder from nigerianfinder.com  520×273 investment options working professional capitalworx advisers from www.capitalworx.in

520×273 investment options working professional capitalworx advisers from www.capitalworx.in  559×921 aggressive investment strategy interesting from investmentbusinessideas.blogspot.com

559×921 aggressive investment strategy interesting from investmentbusinessideas.blogspot.com