Hyperinflation, an economic phenomenon characterized by extremely rapid and out-of-control increases in prices, presents a unique and often perilous environment for real estate investment. While real estate is often touted as a hedge against inflation, its performance during hyperinflation is far from guaranteed and requires careful navigation.

On the surface, the appeal seems logical. As the value of currency plummets, hard assets like property should, in theory, retain or even increase their value in nominal terms. Land and buildings represent tangible wealth, a haven when paper money is losing its purchasing power daily, or even hourly. Demand for real estate might surge as individuals and businesses seek to convert rapidly depreciating cash into something more durable.

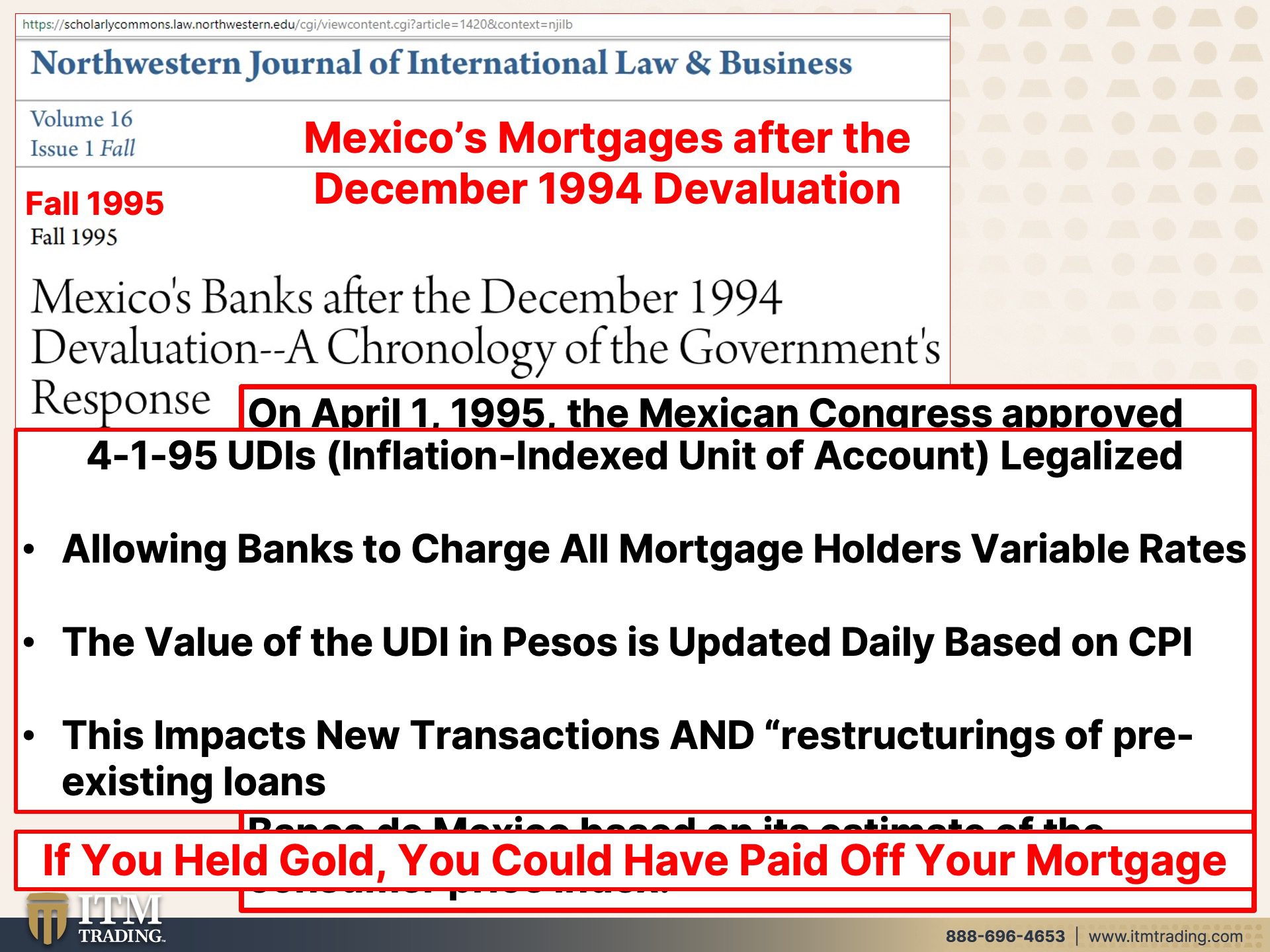

However, the reality is considerably more complex. Firstly, hyperinflation often cripples credit markets. Banks become hesitant to lend due to the uncertainty surrounding future currency values and repayment risks. This scarcity of financing makes it difficult for potential buyers to obtain mortgages, dampening demand even with the urgency to escape currency devaluation. Existing mortgages, while seemingly advantageous with fixed nominal payments, can become virtually worthless to the lender, further discouraging lending.

Secondly, the overall economic instability associated with hyperinflation creates widespread uncertainty. Businesses struggle to price goods and services, impacting profitability and potentially leading to layoffs. This economic downturn can suppress demand for both residential and commercial real estate. Renters may struggle to afford rent increases, and businesses may downsize or close, leaving vacant properties. Therefore, while nominal property values might rise rapidly, real values (adjusted for inflation) could stagnate or even decline.

Thirdly, hyperinflation often triggers government intervention. To control runaway prices, governments might implement price controls on rent or even seize assets, including real estate, under the guise of national security or economic stability. This government interference introduces significant political risk and erodes property rights.

Furthermore, accurately pricing real estate becomes a monumental challenge. Historical data becomes irrelevant as the value of currency changes drastically within short periods. Investors must rely on speculation and potentially unreliable forecasts, making it extremely difficult to determine a fair market value.

Despite these challenges, opportunities may arise for sophisticated investors with deep pockets and a high-risk tolerance. Distressed sales of properties due to bankruptcies or forced liquidations could present bargains. Investing in land outside major urban areas, where there’s potential for future development after the hyperinflation subsides, could also be a strategic play. However, these strategies require a thorough understanding of the local market, political landscape, and a willingness to accept substantial risks.

In conclusion, while real estate might seem like a safe haven during hyperinflation, it is not a guaranteed profit generator. The complex interplay of factors such as credit market dysfunction, economic instability, government intervention, and pricing uncertainty makes real estate investment in hyperinflationary environments incredibly challenging and requires a cautious and informed approach.

960×524 relationship hyperinflation real estate from willowdaleequity.com

960×524 relationship hyperinflation real estate from willowdaleequity.com  637×610 awesome real estate investments hyperinflation from www.investmentwatchblog.com

637×610 awesome real estate investments hyperinflation from www.investmentwatchblog.com  1000×667 hyperinflation real estate impact from mykukun.com

1000×667 hyperinflation real estate impact from mykukun.com  474×315 real estate investment hyperinflation nigerians diaspora from prestigerealestatenews.com

474×315 real estate investment hyperinflation nigerians diaspora from prestigerealestatenews.com  640×427 real estate hyperinflation expert guide from parentportfolio.com

640×427 real estate hyperinflation expert guide from parentportfolio.com  528×650 inflation hyperinflation real estate from www.abcbullion.com.au

528×650 inflation hyperinflation real estate from www.abcbullion.com.au  1463×732 investment hyperinflation from quadrawealth.com

1463×732 investment hyperinflation from quadrawealth.com  1060×446 real estate investment inflation from www.steps.com.qa

1060×446 real estate investment inflation from www.steps.com.qa  591×353 effects hyperinflation real estate industry pakistan from winstonmall.com

591×353 effects hyperinflation real estate industry pakistan from winstonmall.com  1000×673 investing real estate inflation decision from jcomforthomes.co.ke

1000×673 investing real estate inflation decision from jcomforthomes.co.ke  768×512 real estate development business from learn.rajjha.com

768×512 real estate development business from learn.rajjha.com  1640×924 hedge inflation real estate investment types from yourkeytostaugustine.com

1640×924 hedge inflation real estate investment types from yourkeytostaugustine.com  1200×480 understanding inflation impact real estate investing from www.hendersoninvestmentgroup.com

1200×480 understanding inflation impact real estate investing from www.hendersoninvestmentgroup.com  736×1104 hedge inflation real estate investment types from www.pinterest.com

736×1104 hedge inflation real estate investment types from www.pinterest.com  1024×1024 investment spending hyperinflation from retiregenz.com

1024×1024 investment spending hyperinflation from retiregenz.com  883×500 perils personal investment scams hyperinflation from www.marketcollapse.com

883×500 perils personal investment scams hyperinflation from www.marketcollapse.com  1920×1440 real estate drops pt mortgage hyperinflation from www.itmtrading.com

1920×1440 real estate drops pt mortgage hyperinflation from www.itmtrading.com  800×420 real estate investment inflation uncertainty from manahilestate.com

800×420 real estate investment inflation uncertainty from manahilestate.com  940×788 real estate inflation hedge archives norada real estate investments from www.noradarealestate.com

940×788 real estate inflation hedge archives norada real estate investments from www.noradarealestate.com  1362×817 rise real estate inflation from www.valuewalk.com

1362×817 rise real estate inflation from www.valuewalk.com  1200×628 real estate investment hedge inflation rising interest rates from www.singsaver.com.sg

1200×628 real estate investment hedge inflation rising interest rates from www.singsaver.com.sg  1280×720 real estate good investment inflation from propakistani.pk

1280×720 real estate good investment inflation from propakistani.pk